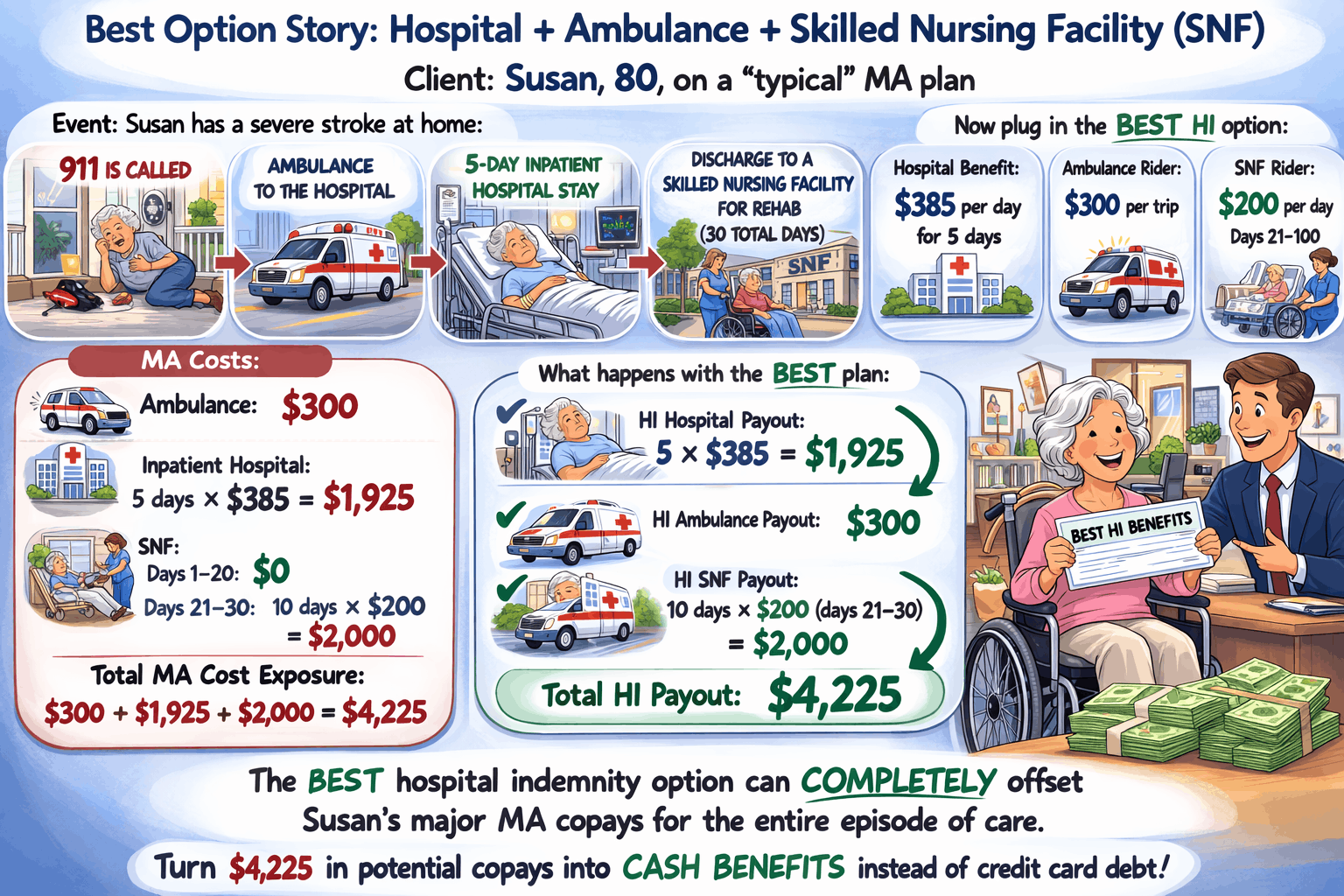

Welcome to our Medicare GLP-1 Bridge program agent blog post. As an independent agent, you’ve probably fielded more than a few phone calls lately from clients stressing over the sky-high costs of weight-loss medications like Wegovy or Zepbound. It’s a tough conversation when you have to explain that standard Part D plans historically haven’t covered these drugs strictly for weight loss, leaving seniors footing a bill upwards of $1,000 a month.

But there is some great news you can finally share with your book of business. The new Medicare GLP-1 Bridge program is officially here, and it’s a massive win for your Part D and MAPD clients.

Launched on July 1, 2026, this time-limited CMS initiative allows eligible Medicare beneficiaries to access select GLP-1 medications for a predictable $50 per month out-of-pocket cost. This is a tremendous opportunity for you to step in, deliver immediate financial relief, and solidify your role as a trusted advisor.

Who Qualifies? Understanding the Clinical and BMI Rules

Before you start calling your book of business, it’s crucial to understand exactly who qualifies. The Medicare GLP-1 Bridge program has strict clinical eligibility guidelines tied to a client’s Body Mass Index (BMI). To get approved, your client must meet one of the following criteria:

-

BMI of 35 or higher: Automatically qualifies for weight-loss coverage without needing a secondary health condition.

-

BMI of 30 or higher: Qualifies if they also have a diagnosis like heart failure (with preserved ejection fraction), uncontrolled high blood pressure, or chronic kidney disease (Stage 3a or higher).

-

BMI of 27 or higher: Qualifies if they have a history of prediabetes, a past heart attack, a past stroke, or symptomatic peripheral artery disease.

Agent Pro-Tip: This program is designed strictly for weight loss. If your client has Type 2 diabetes or moderate-to-severe sleep apnea, they actually do not qualify for the Bridge program because their regular Part D or MAPD plan should already cover their GLP-1 medication!

Partner With Us to Master GLP-1 Bridge Program

Keeping up with sudden CMS rollouts, new clinical BMI rules, and shifting coverage can feel like trying to drink from a firehose. That’s where we come in. Here at Senior Benefit Services, we believe you shouldn’t have to figure out these massive industry shifts on your own. When you partner with us, you get a dedicated team in your corner.

Here is how we help you capitalize on this opportunity:

-

Top-Tier Carrier Portfolio: We provide access to the top-rated Medicare Advantage (MAPD) carriers. You will always have the most competitive plans in your bag to ensure your clients have the foundational coverage they need to access the Medicare GLP-1 Bridge program. We also offer high-value niche products like Hospital Indemnity and Dental/Vision/Hearing (DVH) to help you round out their coverage and increase your per-client revenue.

-

Unmatched Back-Office Support: With decades of experience in the senior market, our specialized underwriting support team is here to help you cut through the administrative clutter so you can spend your time actually selling.

-

Expert Mentorship: We know the senior market inside and out.

The Medicare GLP-1 Bridge program is a demonstration running through December 31, 2027. Now is the time to reach out to your clients, review their prescription drug coverage, and guide them through their options.

For more information, visit the CMS Website