If you’re selling Medicare Advantage but not consistently offering hospital indemnity plans, you’re leaving both your clients and your commissions exposed. Medicare Advantage copays, daily hospital charges, and unexpected out-of-pocket costs can blindside seniors who thought they were “fully covered.” Cross selling hospital indemnity with Medicare Advantage is one of the simplest ways to fill those gaps, protect your clients’ finances, and grow your Medicare book of business with every enrollment. Hospital Indemnity sales are rising every year, but are you just sitting on the sideline?

Why Every Medicare Advantage Agent Should Lead With Hospital Indemnity

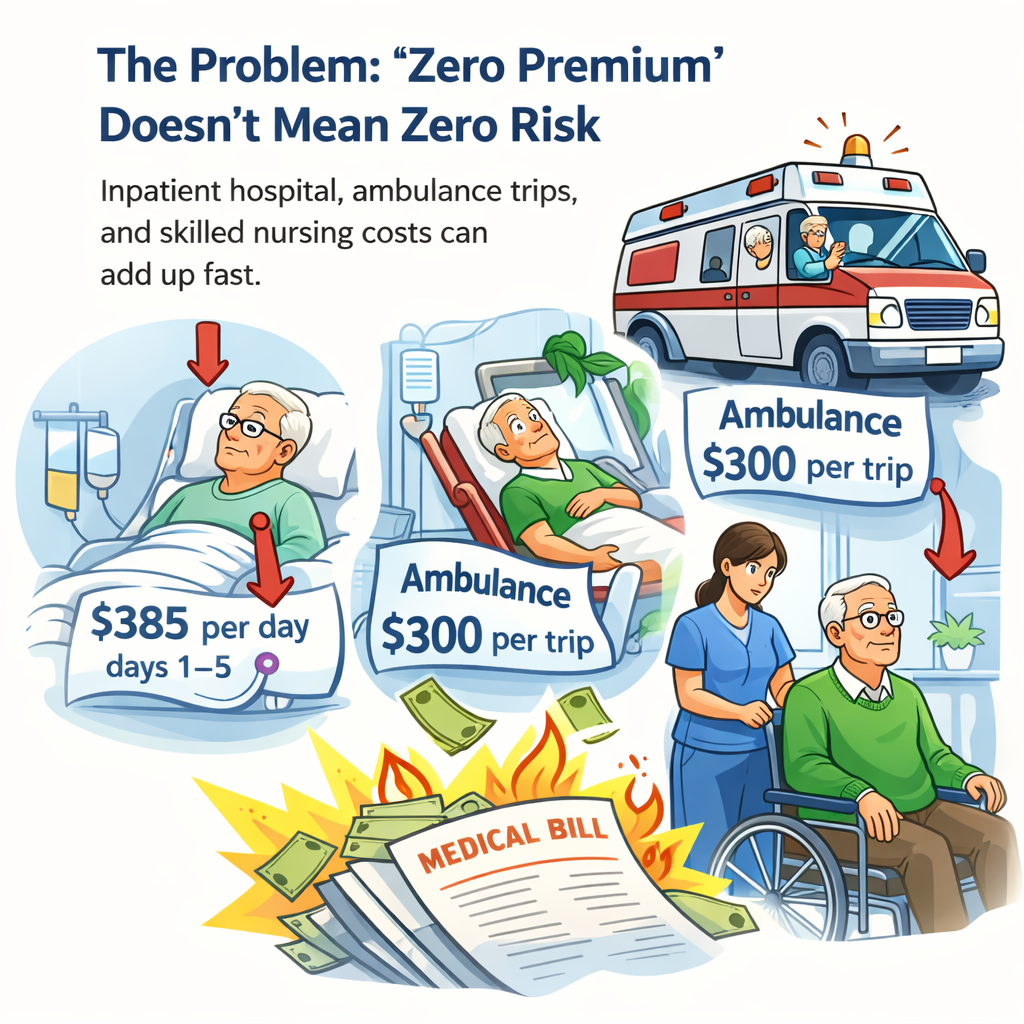

Medicare Advantage plans are popular because they trade a low (or $0) premium for pay‑as‑you‑go cost sharing. That looks great on paper—until a client actually uses the plan and runs into daily hospital copays, an expensive ambulance ride, or a long skilled nursing stay.

A well-designed hospital indemnity (HI) plan can turn those unpredictable copays into predictable benefits, giving your clients real protection and giving you a simple, compliant cross‑sale that adds revenue without adding pressure.

The Problem: “Zero Premium” Doesn’t Mean Zero Risk

Most “typical” Medicare Advantage plans today follow a similar pattern:

-

Inpatient hospital: around $385 per day, days 1–5

-

Ambulance: flat $300 per trip

-

Skilled Nursing Facility (SNF): $0 for days 1–20, then $200 per day for days 21–100

On a rate sheet, those numbers look manageable. In real life, they often hit all at once—after a fall, a heart event, or a serious illness—when your client is least able to handle a bill.

That’s exactly where a simple Good/Better/Best hospital indemnity strategy can shine.

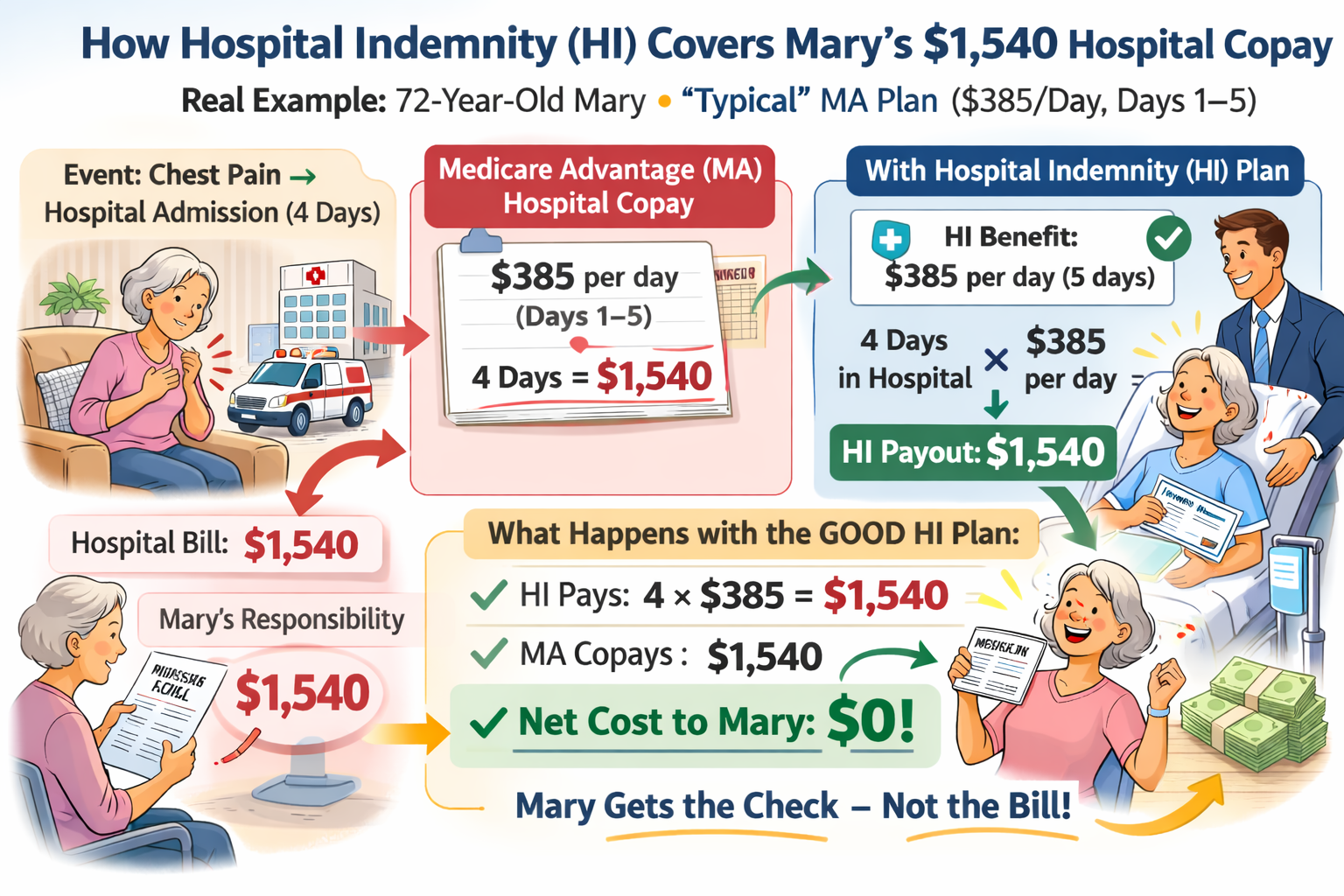

Good Option Story: Covering the Hospital Copay Only

Client: Mary, 72, on a “typical” MA plan

-

Inpatient copay: $385 per day, days 1–5

-

No HI plan yet

Event: Mary has chest pain and is admitted for observation that turns into a 4‑day inpatient stay.

-

MA inpatient cost: 4 days × $385 = $1,540 in hospital copays

Now let’s plug in your Good HI option:

-

HI benefit: $385 per day for 5 days of confinement

What actually happens with the Good plan:

-

Mary’s 4‑day stay triggers 4 HI payments of $385 each

-

HI payout: 4 × $385 = $1,540

-

Her MA hospital copays: $1,540

Net effect: Mary has essentially $0 net cost for the hospital stay (ignoring any other Part B copays or drugs), and she’s the one getting a check from the indemnity policy rather than a surprise bill from the hospital.

With just the Good option, you’ve turned your client’s biggest MA exposure—the daily hospital copays—into a fully funded event. If you’re selling the MA plan, you’re halfway done. The hospital indemnity plan completes the job.

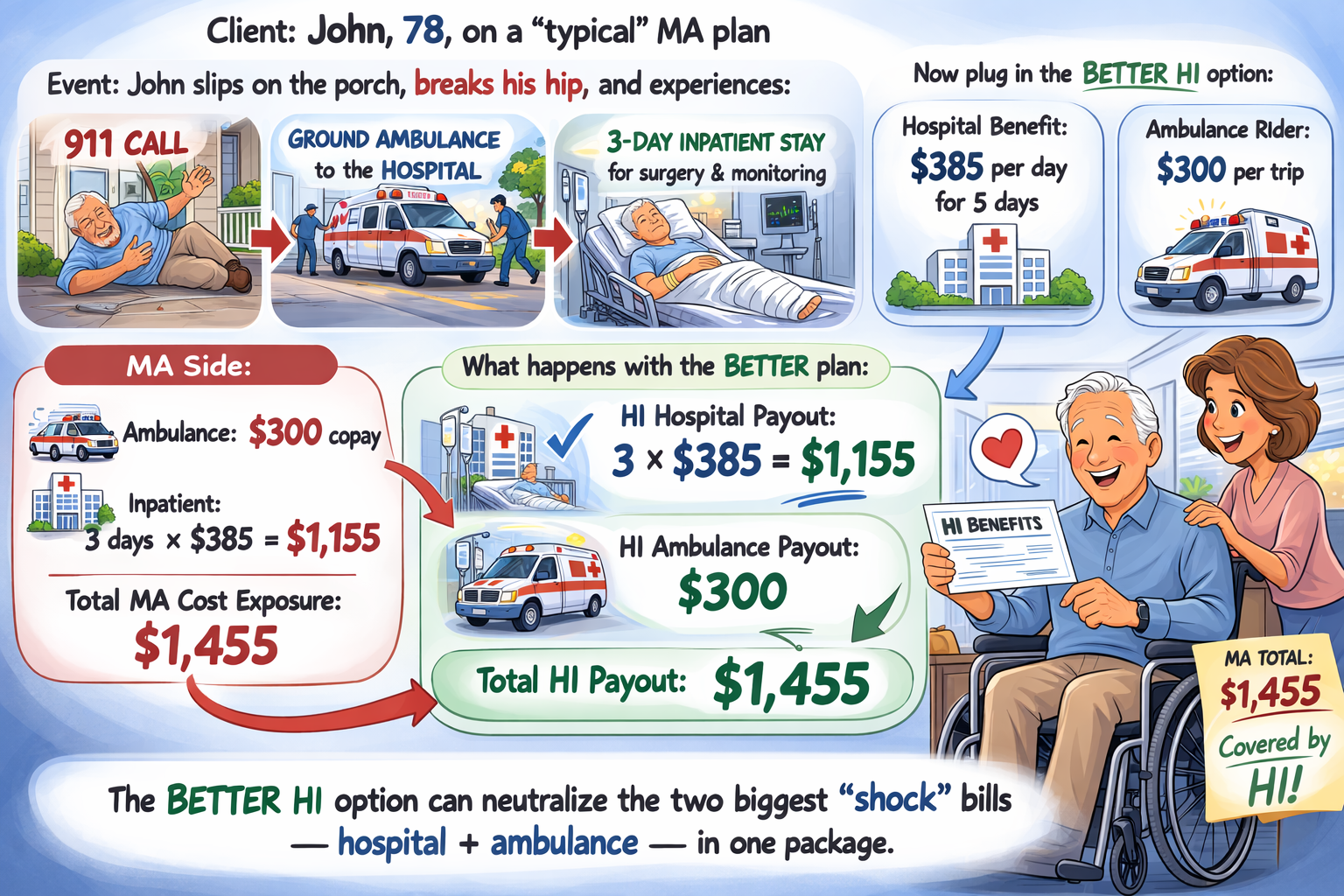

Better Option Story: Hospital + Ambulance Protection

Client: John, 78, on a typical MA plan

-

Inpatient copay: $385 per day, days 1–5

-

Ambulance copay: $300 per trip

Event: John slips on the porch, breaks his hip, and experiences:

-

911 call → ground ambulance to the hospital

-

3‑day inpatient stay for surgery and monitoring

MA side:

-

Ambulance: $300 copay

-

Inpatient: 3 days × $385 = $1,155

-

Total MA cost exposure: $1,455

Now plug in the Better HI option:

-

Hospital benefit: $385 per day for 5 days

-

Ambulance rider: $300 per trip

What happens with the Better plan:

-

HI hospital payout: 3 × $385 = $1,155

-

HI ambulance payout: $300

-

Total HI payout: $1,455

This mirrors John’s total MA exposure for the event. Again, real life may include other minor costs, but your story for agents is simple: the Better HI option can neutralize the two most common “shock” bills—hospital and ambulance—in one package.

The Better option is easy to present: ‘We’ll match the hospital copay, and we’ll also cover your $300 ambulance ride.’

Remember, you aren’t trying to oversell; you’re simply aligning the indemnity benefits with the exact copays printed on the MA Summary of Benefits.

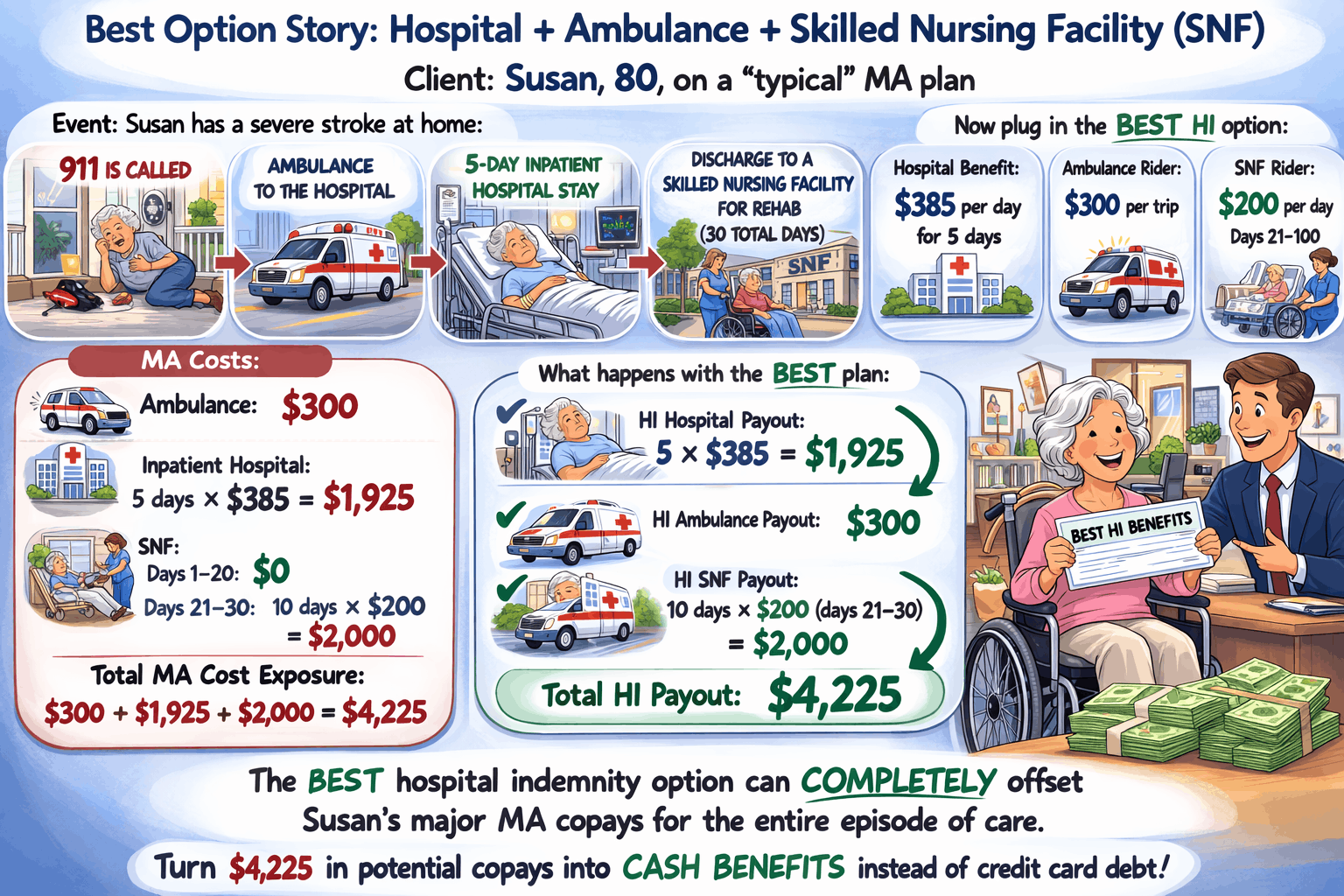

Best Option Story: Hospital + Ambulance + Skilled Nursing Facility (SNF)

Client: Susan, 80, on a typical MA plan

-

Inpatient hospital: $385 per day, days 1–5

-

Ambulance: $300 per trip

-

SNF: $0 days 1–20, then $200 per day days 21–100

Event: Susan has a severe stroke at home:

-

911 is called → ambulance to the hospital

-

5‑day inpatient hospital stay

-

Discharge to a Skilled Nursing Facility for rehab, 30 total days

MA costs:

-

Ambulance: $300

-

Inpatient hospital: 5 days × $385 = $1,925

-

SNF:

-

Days 1–20: $0

-

Days 21–30: 10 days × $200 = $2,000

-

-

Total MA cost exposure:

-

$300 + $1,925 + $2,000 = $4,225

-

Now plug in the Best HI option:

-

Hospital benefit: $385 per day for 5 days

-

Ambulance rider: $300 per trip

-

SNF rider: $200 per day, days 21–100

What happens with the Best plan:

-

HI hospital payout: 5 × $385 = $1,925

-

HI ambulance payout: $300

-

HI SNF payout: 10 days × $200 (days 21–30) = $2,000

-

Total HI payout: $4,225

In this scenario, the Best hospital indemnity option can completely offset Susan’s major MA copays for the entire episode of care.

A stroke isn’t just ‘a hospital stay’—it’s the hospital, the ambulance, and a long rehab. If you only sell the MA plan, you leave your client exposed to over $4,000 in potential copays on a single event. With the Best hospital indemnity package, you give them a way to turn that into cash benefits instead of credit card debt.

How to Present Good/Better/Best to Your Clients

-

“Good” – Hospital only

-

Position: “At a minimum, let’s take the hospital copays off the table.”

-

-

“Better” – Hospital + Ambulance

-

Position: “Most emergencies start with a 911 call. Let’s cover that too.”

-

-

“Best” – Hospital + Ambulance + SNF

-

Position: “If you ever need extended rehab, this keeps daily bills from piling up.”

-

Don’t Leave Your Client Exposed

If you’re writing Medicare Advantage without a hospital indemnity option, you’re doing the hard part and leaving the easy, high‑value protection on the table. Let us show you exactly how to plug this Good/Better/Best model into your current MA presentations and increase both client protection and your revenue per household. Cross selling hospital indemnity with Medicare Advantage plans should always be top of mind.

Contact our Marketing Department today at (800)924-4727 or online to learn how you can not only protect your Medicare Advantage clients with a hospital indemnity plan, but also how you can offset diminishing Medicare Advantage commissions!