The Freedom to Recover at Home: Why a “Full” Medicare Plan May Still Leave You at Risk

Most of our clients share a common goal: staying in their own homes as long as possible. The reality is that even with Medicare and a Supplement this is hard to accomplish. Why??

The Reality Check

While Medicare and Supplements provide excellent coverage for doctors and hospitals, they are notoriously strict when it comes to Home Health Care. To get Medicare to pay for care at home, you typically have to be “homebound,” and the care must be “skilled” and “intermittent.”

Here’s the clean way to look at home health care under Medicare – because this is one of those areas that sounds simple, but can turn into a mess real quick if you don’t understand the rules.

First, Medicare is not going to cover full-time home care.

That doesn’t fly.

They will only consider it if it’s part-time or intermittent, which means:

- Less than 7 days per week

- Or daily care, but under 8 hours per day, and only for up to 21 days

So right out of the gate, this is limited coverage.

Now, on top of that, you have to check every single one of these boxes:

- You’re under a doctor’s care, and they’ve created a plan that they are reviewing regularly

- A doctor confirms you need skilled nursing care (not just basic help like drawing blood)

- A doctor confirms you need therapy services – physical therapy, speech therapy, or continued occupational therapy

- The home health agency must be Medicare-certified

- A doctor must certify that you are homebound

Miss one of these, and Medicare is not paying.

Now let’s talk about the therapy piece, because this is where people get tripped up.

Medicare will only cover those services if they meet very specific standards:

- The care must be medically necessary and safe for your condition

- It has to be reasonable in amount and frequency

- It must be something that only a qualified professional can do

And then one of these must also be true:

- Your condition is expected to improve in a reasonable timeframe

- A skilled therapist is needed to set up a maintenance program

- A skilled therapist is needed to perform that maintenance safely

Bottom line:

This is not long-term care coverage.

This is short-term, medically necessary care with a lot of guardrails.

If you’re thinking Medicare is going to cover extended home care while your client recovers or ages in place, that’s where both agents and consumers get themselves into trouble.

But what if your client just needed help with the basics—like bathing, dressing, or meal preparation—so they could focus on getting stronger? This is where the “Invisible Gap” lives, and it’s where most seniors are forced to dip into their hard-earned savings.

Short-Term Home Health Care: Your Safety Net for Independence

Short Term Home Health Care (STHHC) insurance plans are designed specifically to give your client options. It’s a simple, powerful addition to their portfolio that ensures if they face an illness or injury, the financial burden of recovery doesn’t fall on their family.

Key Benefits of a Short-Term Plan:

-

No “Homebound” Requirement: They don’t have to be confined to your house to trigger benefits. If they need help, they get help.

-

Custodial Care Coverage: Unlike Medicare, these plans cover “Activities of Daily Living” (ADLs). This means someone can be there to help your client with the things that actually allow them to stay home safely.

-

Cash Benefits Paid to Your Client: Most plans pay a daily cash benefit directly to the client, not the provider. They get to decide how to spend it—whether it’s for a home health aide, a therapist, or even a friend or family member helping out.

-

Simple Qualification: Unlike traditional Long-Term Care insurance, which can have a grueling amount of health questions, STHHC plans often have just a few “Yes/No” health questions.

The “Net-Zero” Strategy: Let Your Prescriptions Pay for Your Protection

At Senior Benefit Services, we specialize in a unique financial strategy that many agents overlook.

Many of the top-rated Short-Term Home Health Care plans include a Prescription Drug Reimbursement Benefit.

The Math is Simple:

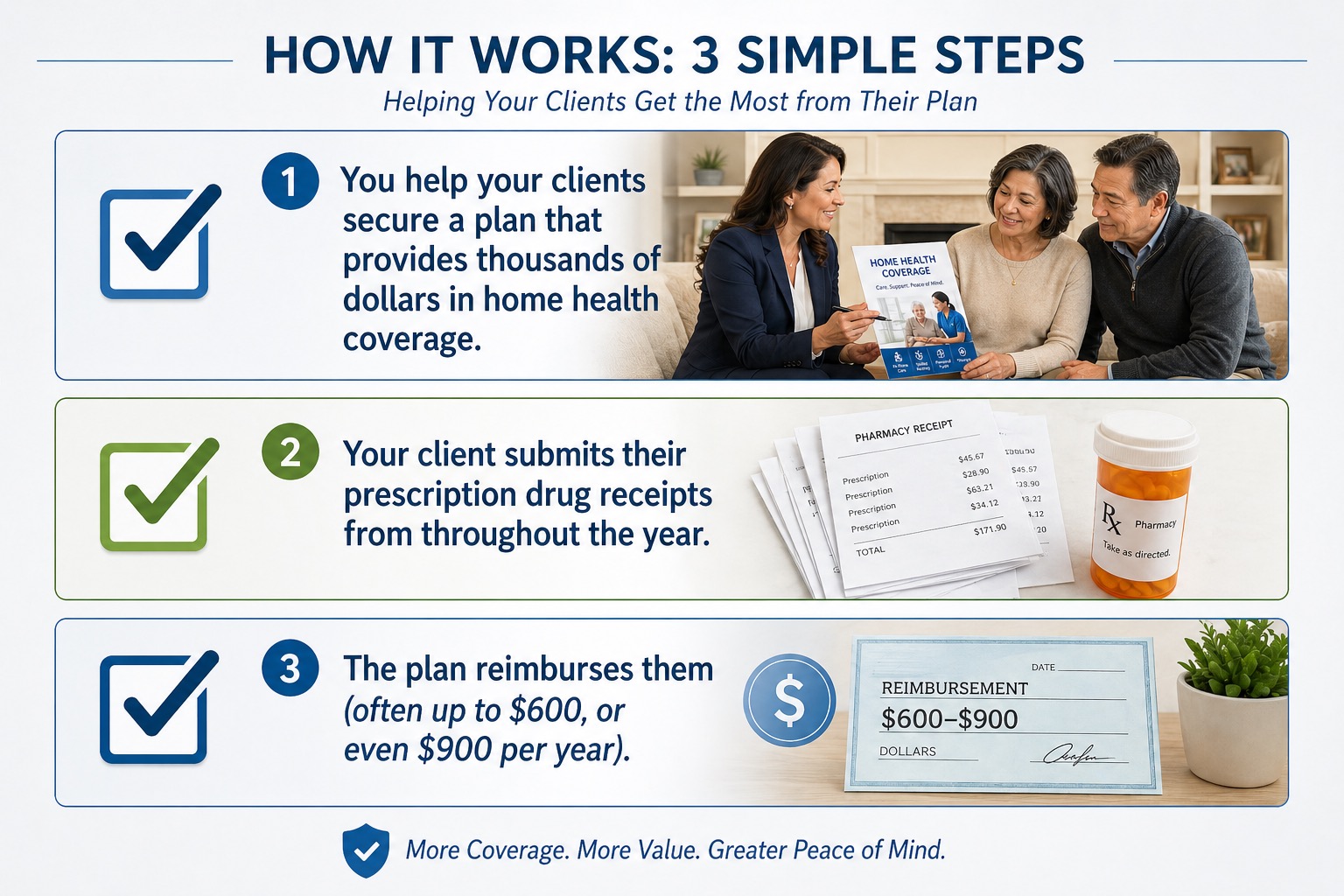

-

You help your clients secure a plan that provides thousands of dollars in home health coverage.

-

Your client submits their prescription drug receipts from throughout the year.

-

The plan reimburses them (often up to $600, or even $900 per year).

For many of your clients, the yearly reimbursement is enough to completely offset the cost of the insurance premium. They gain the security of a home health care plan, and the plan essentially pays for itself through the medicine they were already going to buy.

Is Their Current Plan Enough?

Take a moment to ask yourself: If your client needed help around the house for 6 months while recovering from a surgery, who would pay for it?

-

If the answer is “their kids,” they’re putting a burden on them.

-

If the answer is “their savings,” they’re shrinking their future income safety net.

-

If the answer is “short term home health care,” they’re protected.

Get Your Clients Protected and Earn More in the Process

Our team doesn’t just push contracts; we build blueprints to help you succeed in the senior market. We will compare the top plans in your area to find the one where the prescription reimbursement math works best for your client’s budget. Contact our Marketing Department today at (800)924-4727.